Sally C. Pipes Published 10:30 p.m. ET Oct. 17, 2019

The number of uninsured Americans rose in 2018 for the first time since the Affordable Care Act passed in 2010, according to recent research from the Census Bureau.

Obamacare’s defenders were quick to blame the change on meddling by the Trump administration. But the real culprit is the law’s faulty design.

Since the first exchange plans went into effect in 2014, Obamacare has consistently delivered higher premiums and deductibles for average Americans who don’t get coverage from their employers. As a result, millions of people have fled the Obamacare exchanges over the past few years. Today, only people who receive government subsidies can afford exchange plans.

Currently, Americans who make less than 400% of the federal poverty level but do not qualify for Medicaid are eligible for subsidies for Obamacare plans. These subsidies are often quite generous. For example, a family of four with $50,000 in annual income could get a $15,855 plan for just $3,250 — or $271 per month.

Just under half of Americans are eligible for these subsidies. The rest are out of luck, and face monthly premiums routinely exceeding $1,000.

As a result, many people are deciding not to shop for coverage on Obamacare’s exchanges. Between 2016 and 2018, unsubsidized enrollment plummeted by 2.5 million — a 40% decline from around 6.2 million to 3.7 million. Eighty-seven percent of people with exchange coverage received subsidies in 2019.

The cost of exchange coverage has soared because of Obamacare’s many rules, mandates and regulations. For instance, Obamacare requires every plan sold on the exchanges to cover a list of 10 “essential health benefits,” from pediatric vision care to substance abuse treatment. Such comprehensive coverage is expensive. It’s also unappealing to many people, particularly young folks for whom these benefits seem far from “essential.”

Obamacare also forces insurers to charge everyone of a certain age the same rate, regardless of their health status or history. On top of that, it prevents insurers from charging older enrollees more than three times as much as younger enrollees.

Mandates in the Affordable Care Act have resulted in higher costs for insurers, which they’ve passed on to enrollees in the form of higher premiums, Pipes writes. (Photo: Shawn Fury, VA Eastern Colorado Health Care System)

These mandates have raised costs for insurers, which they’ve passed on to enrollees in the form of higher premiums. In 2017, average exchange premiums rose 21%. Not surprisingly, exchange enrollment fell by 10 percent that same year. Americans who didn’t qualify for subsidies accounted for roughly 85% of this decrease.

An additional 1.2 million unsubsidized patients exited the exchanges in 2018, when premiums rose by 26%.

Some states saw particularly alarming coverage drops. From 2016 to 2018, unsubsidized exchange enrollment in Arizona, Iowa, Georgia, Nebraska, Oklahoma and Tennessee plummeted by over 70%.

That trend is almost certain to continue as marketplace premiums keep rising. Next year, exchange premiums for Vermont’s Blue Cross Blue Shield patients will jump 12%, on average. In New York, average premiums will increase by about 7%; New Mexico’s plans could be 13% more expensive.

Fortunately, there’s at least one option still available to those who can’t afford the plans for sale on Obamacare’s exchanges — short-term, limited duration insurance. These policies are exempt from Obamacare’s mandates. Insurers don’t have to cover every essential health benefit and can price plans based on a beneficiary’s medical risk.

As a result, short-term plans are far more affordable. One analysis found that premiums for the cheapest short-term plans are 80% lower than those for the least expensive Obamacare plans.

And thanks to a recent rule change by the Trump administration, Americans can purchase short-term plans that last up to 364 days. Insurers can also renew those policies for up to three years. Previously, short-term plans only lasted three months and couldn’t be renewed.

As the next open enrollment period approaches, it’s clearer than ever that Obamacare has failed. The law’s mandates were supposed to help every American get insurance. Instead, they’ve made it impossible for almost anyone to purchase coverage without a government subsidy. So much for the “Affordable” Care Act.

Sally C. Pipes is president, CEO and Thomas W. Smith fellow in health care policy at the Pacific Research Institute. Her latest book is “The False Promise of Single-Payer Health Care” (Encounter). Follow her on Twitter @sallypipes.

While both sides of the healthcare debate are rolling out stories of victims to pull on the heartstrings, every American is going to be a loser if ObamaCare isn’t repealed and replaced. I have two children with cystic fibrosis (CF), a genetic disease that ravages the lungs and digestive system, will ultimately shorten my children’s lifespans, and cost a fortune to treat throughout their lives.

This debate has a very real impact on my family. We need good health insurance, just like other families or individuals with pre-existing conditions. But the false promises of ObamaCare have never been the answer.

Legislators and lobbyists in Washington, D.C., can argue for months over how to fix ObamaCare, the healthcare legislation forced through Congress in 2010 under President Obama’s tutelage. He promised the law would cover 23 million people; in actuality, it’s covered less than half of that.

In 2013, Politifact declared President Obama’s pithy ObamaCare pitch, “If you like your health plan, you can keep it,” as the Lie of the Year. Insurers are fleeing the exchanges and states all together. When they aren’t doing that, they are asking for insane rate increases, like the one and only insurer left in Delaware, who asked for a 33.6 percent rate increase for 2018. Residents of Delaware are getting off easy compared to people in Iowa, whose only ObamaCare insurer in the state asked for a rate hike of 43.5 percent. And, next year, it’s projected that 2.4 million Americans will only have one insurer to “choose” from, while 27,000 Americans will have zero options under ObamaCare.

ObamaCare is collapsing and Americans are worried sick about what’s next, especially families like mine, that rely on health insurance to pay for expensive treatment.

While politicians in Washington are arguing about the finer details of ObamaCare, it’s imploding all around the country. Soon, they will have nothing to argue over because ObamaCare won’t exist.

And part of me wonders if that was the plan all along. Step 1: Create an unsustainable quasi-private, quasi-government health coverage that will fail because ObamaCare did nothing to help reduce the costs of healthcare and prescription drugs. Step 2: When ObamaCare fails, con Americans into believing that European-style single payer healthcare is the savior.

And as a parent of two children with life-threatening diseases, this impending implosion of ObamaCare and the subsequent national pitch for single payer health care terrifies me the most. The state would then have the ability to say when they would cut off care to any American.

Look at who President Obama chose for a recess appointment as the head of Center for Medicare and Medicaid Services in 2010, Dr. Donald Berwick. The esteemed doctor actually published papers effectively laying out how the state could ration care to those who were deemed to contribute less to society.

In the UK, baby Charlie Gard’s parents are being told that he will be removed from life support against their wishes and that they are not allowed to move their son out of the hospital to die at home or to take to another country for treatment, even those though they have raised all of the money to pay for it. The state is holding their son hostage.

While I share the concern that Sen. Ted Cruz’s (R-Texas) Better Care Reconciliation Act would cut Medicaid, which 45 percent of CF patientsrely on for some type of coverage to help pay the tens of thousands of dollars each month just for prescription drugs, a single payer health care system is not the way to go.

As Americans, my children are very lucky. They live in a nation that, because of the free market, gives great incentives to drug companies to spend millions of dollars on research to find life-sustaining and life-prolonging treatments. For example, Boston-based Vertex Pharmaceuticals developed Kalydeco and Orkambi, two of the first drugs in the history of the world that correct a specific genetic defect. Those two medicines could add years of life for CF patients.

While the annual costs of these medicines are high, so was the cost of developing them. Are they making millions in profits? I hope so. They took the risk and spent years doing something others have previously failed to do, researching a drug that they knew would only treat about 30,000 Americans. So yes, I hope they are making a hefty load of cash as I pray they go back and keep researching until they find a cure.

Patients in other countries are still waiting for these drugs because their single-payer government health care system won’t pay the high costs.

Watching the wheels of Washington turn is agonizing for parents and patients of deadly and expensive diseases.

And the bottom line is this: Congress needs to uphold President Trump’s promise to repeal ObamaCare and replace it with something better, something that keeps health insurance companies in the game and encourages citizens to pay for private insurance, something that allows those who truly need it to have access to Medicaid benefits, something that helps lower the cost of healthcare with free market reforms, and something that keeps our health care system far, far away from Charlie Gard’s kidnappers in the UK.

Get to work, Congress. Either step up and do your jobs or get out of the way.

A local family will meet with President Trump when he arrives at the Cincinnati airport Wednesday.

Mrs. Raya Mafazy Whalen and her husband, Michael, who live in the Dayton area are the owners of PlayCare, an Ohio-based small business that specializes in the design, sale, installation, and maintenance of commercial playground equipment. PlayCare employs 15 Ohioans and Whalen says given its size and health policy exemptions, some might underestimate the disastrous impact of Obamacare.

According to a statement from the White House Media Affairs Office, prior to the enactment of the Affordable Healthcare Act, the Whalens’ company offered affordable health care options to its employees. The Whalens purchased health care through their own company as well. However, following the ACA enactment, the company’s plan was considered unacceptable by the government due to over burdensome regulations. They and their employees were forced to purchase health insurance through the Affordable Care Act exchanges.

The White House says recently, Raya’s 7-month-old child needed to be hospitalized. The cost of the hospitalization for the child left Raya and her husband with a $5,000 cost.

Raya founded the Young Republican Women of Cincinnati.

Raya will be accompanied by her husband Michael Whalen and their 7-month old baby Colette.

2 NEWS spoke with the Whalens in 2015 during a GOP Presidential Debate.

A second family from Kentucky will also meet with the President to discuss their issues with healthcare as well.

Leslie Kurtz needed three plates, eight screws and a big assist from her insurer after breaking every bone in her ankle while white water rafting.

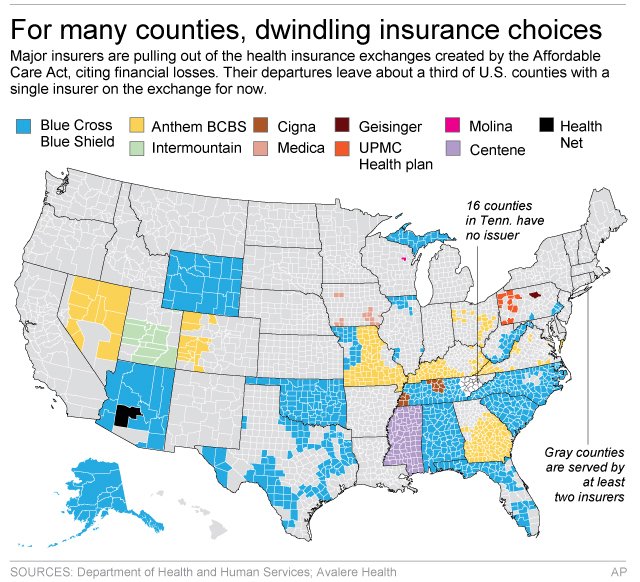

Coverage she purchased through a public insurance exchange established by the federal health care law paid $65,000 toward surgery and the care she needed after the 2015 accident. But that protection may not exist next year because insurers have abandoned the Knoxville, Tennessee resident’s exchange. As of now, Kurtz has no future coverage options, and she is worried.

“I can’t afford to have everything I’ve worked for taken away because I fell down the steps,” Kurtz said.

Her county is one of 16 in Tennessee that lack even a single insurance company committed to offering coverage for 2018 on the exchange, after Humana announced last month plans to exit.

Exchanges set up by the Affordable Care Act were designed to give customers a chance to shop for coverage and then buy a plan, most with help from tax credits. The idea was that such a marketplace would push insurers to offer affordable plans to compete for customers.

But insurers in many markets have been pulling back from the exchanges after losing money. According to an analysis by the Associated Press and the health care firm Avalere Health, more than 1,000 counties, where about 2.8 million people are insured through the exchanges, are down to their last insurance carrier, according to the most recent data.

With less competition, that could mean sharply higher rates. And with more insurers still considering leaving other markets, customers around the country could be stuck like Kurtz with no affordable coverage options in 2018.

County-level data for health insurance providers under the Affordable Care Act.

Insurers still have a few more weeks to decide to stay in their exchanges, and other insurers may jump into new markets, though that can be expensive and risky for them. The government recently announced several short-term fixes for the exchanges, and insurers have welcomed the moves. But they want to see the final version of the improvements before deciding on 2018.

“No insurer wants the negative public backlash from dropping insurance for lots of people, but the companies need to feel like the market is stable and that there’s a chance of making money,” said Larry Levitt, a health insurance expert with the nonprofit Kaiser Family Foundation.

Chief among undecided companies is the Blue Cross-Blue Shield carrier Anthem Inc. It is the lone insurer on exchanges in 300 counties in seven states, according to data compiled by the AP and Avalere.

Anthem CEO Joseph Swedish would not commit to participating on exchanges next year and said in a statement last month that the market is sliding toward “significant deterioration and requires changes to ensure future stability and affordability.”

Anthem and the many other companies that sell coverage under the Blue Cross-Blue Shield brand will be crucial to the fate of the exchanges because they often specialize in insurance for individuals, and many have a long-standing presence in their markets. They also are the only remaining option on exchanges in nearly a third of the nation’s 3,100 counties.

For instance, Blue Cross and Blue Shield of North Carolina is the lone exchange option in 95 counties, covering more than 500,000 people, according to the analysis by AP and Avalere. The North Carolina insurer, which is not owned by Anthem, declined to comment on its 2018 plans.

Insurers typically are still sorting out coverage plans at this time of year, so it’s not unusual for them to be undecided about 2018. But never before have insurers bluntly stated that they can’t commit until they see what the government does to improve the exchanges.

The Kaiser Family Foundation’s Levitt says insurers are worried about losses, but they also may be using the leverage their indecision gives them.

“Insurers kind of want the threat that they may pull out to be taken seriously now, so that they get some of the changes they are looking for,” he said.

Customers can buy coverage outside the exchanges, if insurers are selling individual plans in their market. But then they won’t be able to use tax credits to help pay the bills, which may be particularly painful since many markets have seen prices soar.

Customers won’t know for certain who is selling on their exchanges until next fall. While insurers have to apply to sell coverage on their exchanges generally by late spring or early summer, they can drop out later if claims turn out worse than expected, noted Dave Dillon, a fellow of the Society of Actuaries.

Last fall, Blue Cross and Blue Shield Nebraska announced a little more than a month before open enrollment started that it was shuttering its exchange business due to a loss of $140 million.

Insurance experts have said bigger metropolitan areas usually have more choice on their exchanges. But smaller cities or rural areas could be hurt most if more insurers pull back.

Customers who already lost exchange options for 2018 are concerned. Knoxville resident Melissa Nance bought her Humana plan on the exchange without a subsidy, but she’s worried that she won’t find an affordable replacement after that insurer leaves.

The 45-year-old is fighting an aggressive form of leukemia. She needs insurance to cover blood tests and CT scans to detect whether the cancer has returned.

“I’m a sick person now,” she said. “I am constantly having to go to the doctor.”

Fellow Knoxville resident Leslie Kurtz is thinking about moving. The self-employed television producer needs subsidies to afford coverage for her family of four.

Kurtz says she would have gone bankrupt if she had no insurance when she broke her ankle.

“I don’t have $65,000, I would have had to sell the house,” she said. “We need access to health care because (stuff) happens.”

Right now, many people are focused on the details of the plan that will replace ObamaCare after it is repealed.

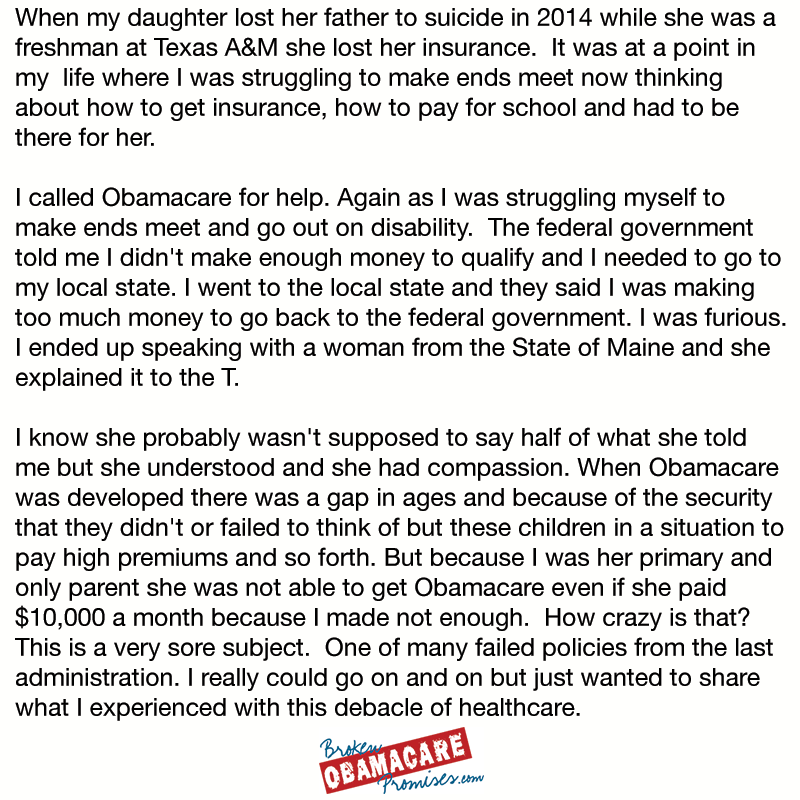

But let’s not put the cart before the horse here. First, we still need to repeal ObamaCare. And why? Because it’s hurting millions of Americans. People like Susie from California. Here’s her story:

Not only is Susie’s monthly premium under Obamacare more expensive than her mortgage, her insurance (Covered California) has repeatedly fought her for every procedure, ER visit and doctor bill she has incurred. Worst of all, Susie has an arrhythmia problem but cannot get the cardiac rehab she needs despite a recent incident of incapacitating palpations which lasted for a day and a half. Susie says she truly doesn’t think her insurance cares if she lives or dies. In her words, “It’s sick to be treated like an unworthy person when you are so sick.”

At BrokenObamaCarePromises.com, we’ve been collecting stories of the true human cost of ObamaCare. If ObamaCare has caused your insurance premiums to spike, or caused your policy to be cancelled, we want to hear from you. Share your story by emailing us at mystory@brokenobamacarepromises.com. Pictures and/or video testimonials are encouraged.

Republicans are nervous about repealing ObamaCare’s supposed ban on discrimination against patients with pre-existing conditions. But a new study by Harvard and the University of Texas-Austin finds those rules penalize high-quality coverage for the sick, reward insurers who slash coverage for the sick, and leave patients unable to obtain adequate insurance.

The researchers estimate a patient with multiple sclerosis, for example, might file $61,000 in claims. ObamaCare’s rules let MS patients buy coverage for far less, forcing insurers to take a loss on every MS patient. That creates “an incentive to avoid enrolling people who are in worse health” by making policies “unattractive to people with expensive health conditions,” the Kaiser Family Foundation explains.

To mitigate that perverse incentive, ObamaCare lobs all manner of taxpayer subsidies at insurers. Yet the researchers find insurers still receive just $47,000 in revenue per MS patient—a $14,000 loss per patient.

Predictably, that triggers a race to the bottom. Each year, whichever insurer offers the best MS coverage attracts the most MS patients and racks up the most losses. Insurers that offer high-quality coverage either leave the market, as many have, or slash their coverage. Let’s call those losses what they are: penalties for offering high-quality coverage.

The result is lower-quality coverage—for MS, rheumatoid arthritis, infertility and other expensive conditions. The researchers find these patients face higher cost-sharing (even for inexpensive drugs), more prior-authorization requirements, more mandatory substitutions, and often no coverage for the drugs they need, so that consumers “cannot be adequately insured.”

It doesn’t have to be like this. Employer plans offer drug coverage more comprehensive and sustainable than ObamaCare. The pre-2014 individual market made comprehensive coverage even more secure: High-cost patients were less likely to lose coverage than similar enrollees in employer plans. The individual market created innovative products like “pre-existing conditions insurance” that—for one-fifth the cost of health insurance—gave the uninsured the right to enroll in coverage at healthy-person premiums if they developed expensive conditions.

If anything, Republicans should fear not repealing ObamaCare’s pre-existing-conditions rules. The Congressional Budget Office predicts a partial repeal would wipe out the individual market and cause nine million to lose coverage unnecessarily. And contrary to conventional wisdom, the consequences of those rules are wildly unpopular. In a new Cato Institute/YouGov poll, 63% of respondents initially supported ObamaCare’s pre-existing-condition rules. That dropped to 31%—with 60% opposition—when they were told of the impact on quality.

Republicans can’t keep their promise to repeal ObamaCare and improve access for the sick without repealing the ACA’s penalties on high-quality coverage.

Mr. Cannon is director of health policy studies at the Cato Institute.

Pamela Weldin’s experiences with Obamacare can be boiled down to just a few numbers.

Since the health care law’s implementation three years ago, Weldin, 60, has lost her insurance four different times.

And the Nebraska woman is currently enrolled in her fifth new insurance policy in four years.

“Yet again, and through no fault of my own,” Weldin told The Daily Signal. “I’m just sitting here minding my own business, and here we go again.”

A former dental hygienist, Weldin has all the hallmarks of a consumer intended to benefit from the Affordable Care Act.

She has been denied coverage in the past because of a pre-existing condition related to her career as a dental hygienist.

Additionally, Weldin qualifies for a tax credit, which she has received every year since 2014.

As a result, her premiums are low when compared to consumers who don’t qualify for financial assistance: In early 2015, Weldin purchased a plan through Blue Cross and Blue Shield of Nebraska that cost her $232 each month.

This year, premiums for her silver-level plan with Medica are $161 per month after her tax credit.

But though Weldin has benefited from aspects of the law, she hasn’t been immune to the changes in the health insurance market that have occurred in last few years.

“I’m a person who has been denied because of pre-existing conditions,” Weldin, a Pampered Chef director, said. “I’m on Obamacare and have lost my insurance four times in three years. I understand the challenges, but it’s not sustainable.”

Pamela Weldin of Minatare, Nebraska, lost her insurance four times since the Affordable Care Act took effect in 2014. (Photo: Pamela Weldin)

Weldin’s Journey

Since HealthCare.gov opened for business in the fall of 2013, four policies sold by three different insurance companies—Humana, CoOportunity Health, and Blue Cross and Blue Shield of Nebraska—that Weldin purchased were ultimately terminated.

The Daily Signal previously covered her experiences with Obamacare in a February 2015 article.

But since then—when Weldin lost her insurance for a third time—she’s logged another cancellation.

First, Weldin’s initial policy with Humana, which she held for several years, was canceled in the lead-up to Obamacare’s implementation in January 2014.

The Nebraska woman then purchased a platinum-level plan for 2014 through CoOportunity Health, a consumer operated and oriented plan, or co-op. But CoOportunity Health terminated her platinum-level policy for 2015 after the co-op decided it would no longer offer those policies.

Weldin, though, decided to stick with CoOportunity Health and selected a silver-level plan for 2015.

On Jan. 23, 2015, Weldin received a notice from the co-op notifying her that it was going out of business. CoOportunity far outpaced its initial enrollment projections, and its customers racked up medical expenses that far outpaced what they paid in premiums.

Weldin had no choice but to select a new insurer and policy, and purchased coverage through Blue Cross and Blue Shield of Nebraska for the remainder of 2015 and 2016—a plan that, though a bit more expensive, allowed her to see her original doctor.

Late last year, though, Blue Cross and Blue Shield of Nebraska announced it would no longer sell coverage on the exchange in the state.

“This system is collapsing under its own weight,” Weldin said, “like the co-ops and basic companies like Blue Cross pulling out of Nebraska.”

To ensure she would be covered for 2017, Weldin went to HealthCare.gov to select a plan that allowed her to see her current doctor in Colorado.

In Nebraska, consumers on the exchange had just two insurance companies to choose from: Aetna and Medica.

A policy through Aetna was more expensive than its competitor, but because Weldin thought her doctor was considered in-network, she selected a plan through that insurer.

It wasn’t until after she paid her first month’s premium, however, that Weldin learned from the insurance company that any doctor located more than 100 miles from her rural Nebraska home wasn’t in her network.

If she wanted to see her doctor in Colorado—considered out-of-network now—Weldin had to meet a $20,000 out-of-network deductible before Aetna would start covering her medical expenses.

That information, she said, wasn’t listed on HealthCare.gov when she was shopping for plans.

“$20,000 for a deductible? Are you kidding me?” Weldin said. “How is that affordable?”

From left, Republican Reps. Scott Perry, Jim Jordan, and Raul Labrador spoke about Obamacare repeal at a monthly press Q&A session. (Photo: Tom Williams/CQ Roll Call/Newscom)

Speaking Volumes

Across the country, millions of Americans faced higher premiums heading into 2017.

And premium hikes have been well documented by The Daily Signal and others.

Less attention, however, has been paid to the number of insurers and plans available to consumers.

According to an October report from the Department of Health and Human Services, insurer participation in Nebraska decreased from four insurers in 2016 to two in 2017.

And consumers nationwide aren’t just seeing a decline in the number of insurance companies selling coverage on the exchange in their states.

The federal government reported that Americans would also see a decrease in the number of plans insurers offered in 2017.

In Nebraska, there was an average of 18 fewer plans per county available on the exchange to consumers this year. Nebraskans purchasing plans on HealthCare.gov in 2017 had 13 plans to choose from, down from 31 last year.

“That speaks volumes in terms of ultimate consumer benefits,” Rep. Adrian Smith, R-Neb., told The Daily Signal of the change in insurers selling plans in his state. “Fewer choices most often means higher prices and less quality.”

In 2015, Smith introduced a bill to exempt consumers like Weldin who purchased coverage from a failed co-op from the individual mandate. The legislation passed the House, but stalled in the Senate.

Now, Smith and other Republicans—who have spent six years talking about repealing Obamacare—are looking to check the box on a major campaign promise.

Republicans have taken the initial step toward dismantling the health care law after passing a budget resolution earlier this month, and often cite the experiences of Americans like Weldin to bolster their arguments that Obamacare needs to be repealed and replaced.

But despite their control over Congress and the White House, Republican lawmakers differ on their approaches to unwinding Obamacare.

Conservatives are urging GOP leadership to move forward with repeal as soon as possible and say they’re frustrated with the speed at which their leaders are moving to dismantle the health care law.

House Speaker Paul Ryan said last week repeal would be slated for March or April.

“I’d like to see an acceleration of the front-end repeal side,” Rep. Jim Jordan, R-Ohio, said Wednesday at a monthly gathering with reporters. “Let’s get rid of [Obamacare]. That’s what we told the voters that we were going to do.”

Jordan was joined by other Republicans who said they want to see GOP leadership move faster on Obamacare repeal.

“I, too, am frustrated with the pace,” Rep. Scott Perry, R-Pa., said Wednesday. “We need to not only be against the [Affordable Care Act] or Obamacare, which I am for a myriad of reasons … but we also, if not for political reasons, but for the reason that our constituents and America needs to know what we stand for. We should vote on something.”

But during a gathering last week of House and Senate lawmakers in Philadelphia, other Republicans showed tepid support for dismantling the law and even expressed doubts over their party’s plans to repeal and replace Obamacare.

Though the GOP agrees that the law needs to be scrapped, members haven’t yet concurred on whether to repeal major parts of Obamacare like its taxes. Many also want to see Congress move a replacement at the same time they repeal the law.

Still, Smith, the Nebraska congressman, points to Americans like Weldin as a reason why Congress needs to act.

“When you look at the overall picture, [Obamacare] has failed miserably and will continue to cause great damage,” Smith said. “That’s why we need to step in.”

“We want to prevent further pain that we know will happen if we just let Obamacare sit the way it is,” he continued.

“I’m on Obamacare and have lost my insurance four times in three years,” Pamela Weldin said. “I understand the challenges, but it’s not sustainable.” (Photo: Pamela Weldin)

‘Not Sustainable’

After learning about her $20,000 out-of-pocket deductible, Weldin contacted HealthCare.gov to seek assistance with purchasing another plan.

A representative there was able to enroll her in a new policy with Medica, and Weldin learned that her doctor was, in fact, included in the new plan’s network.

This year, the Nebraska woman will pay $161 per month in premiums after a tax credit.

Weldin is one of the more than 9 million Americans who receives a tax credit and has been relatively immune to the increased costs of health insurance, but she still wants to see changes made to the health care system.

“Allow us the choice of what kind of policy and coverage suits our needs,” she said. “Allow us the choice of deductible and to cross state lines for provider care so we can choose and keep our own doctors. Allow insurance companies to compete across state lines so we have more options and have more choice of providers.”

And Weldin said she recognizes that any action Republicans take on Obamacare could very well lead to further changes with her insurance and the health insurance market.

Still, she said she wants to have additional choices, even it means more coming out of her pocketbook.

“Something has to be done because this is not sustainable,” Weldin said. “I’m fine paying a little bit more if it’s what I need. But let me choose a policy that’s appropriate for my needs. Let me have a policy that’s appropriate to my medical needs. Let me choose a deductible that’s appropriate for my budget.”